$2.59 trillion, 50 million customers

The industry is spending 2.59 trillion dollars a year to etch gen-AI into physical silicon, on the bet that this paradigm is the durable one. The paying base is about 50 million people, the productivity that would pay for it isn't measurable, and no software paradigm has ever been the forever thing.

AI-assisted postDrafted with help from Claude, edited and fact-checked by Mart. See transparency policy →

The tower of the Bank for International Settlements, Basel. In June 2026 the central bank of central banks listed an AI bust among the top threats to the global economy. Photo by Michal Pleskowicz, CC BY-SA 4.0.

{kind=link}

Gartner expects the world to spend $2.59 trillion on AI in 2026, up 47% in a year, much of it going to infrastructure: the servers, the networking, the AI-processing silicon. That is the largest capital bet in the history of technology, and it is a bet about a very specific thing. Not that AI is useful. That AI is the durable workload, the one worth carving into physical hardware that takes years to design and depreciates to nothing in about three years.

So it is worth asking the boring question the buildout depends on: who pays for it?

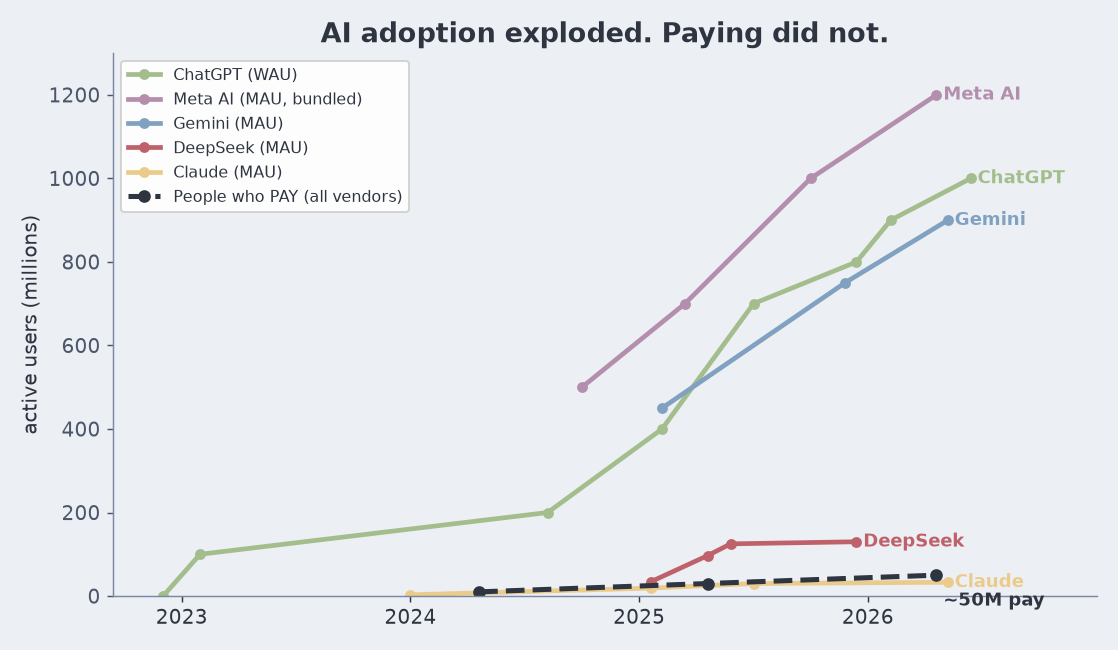

AI adoption by users, against the number who actually pay (ChatGPT counted in weekly actives, the rest monthly; the paying line is a rough all-vendor estimate).

The funnel

Start at the top and walk down.

There are about 6.1 billion people online, roughly 74% of humanity. The other 2.2 billion are not customers of anything digital; they cannot be sold a subscription. That is the ceiling, and the buildout is already priced above it.

Of those online, around a billion use ChatGPT, the fastest consumer product ever to that scale. Impressive, and free. A free user is a cost, not a customer.

Of that billion, about 50 million pay across OpenAI's consumer tiers, part of a company-wide run-rate around $25 billion a year. That is the honest bottom of the funnel: a 5% conversion, and about 0.6% of the human race.

flowchart TD

SPEND["$2.59T spent on AI in 2026"] --> ONLINE["6.1B people are online"]

ONLINE --> USERS["~1B use AI, for free"]

USERS --> PAY["~50M actually pay"]

classDef bet stroke:#ebcb8b,stroke-width:2.5px

classDef thin stroke:#bf616a,stroke-width:2.5px

classDef plain stroke:#7b88a1,stroke-width:2.5px

class SPEND bet

class PAY thin

class ONLINE,USERS plain

The funnel the buildout has to cross, top to bottom. Amber is the bet, red is the base that has to repay it, grey never converts.

Put the two ends together, and mind the order of magnitude: the $2.59 trillion is industry-wide while the 50 million is OpenAI's own count, so read the distance as a rough ratio, not a precise one. Even so, the leading AI company's entire revenue, about $25 billion, is roughly 1% of a single year's industry AI spend. Charge every one of those 50 million subscribers, let nobody churn, and you are still collecting a few hundred dollars a year each against a bill of $2.59 trillion. The revenue is not close to the capital, and the capital resets every hardware generation.

And that capital is not holding still. It is compounding at a rate ordinary companies never sustain, and it does not stop in 2026.

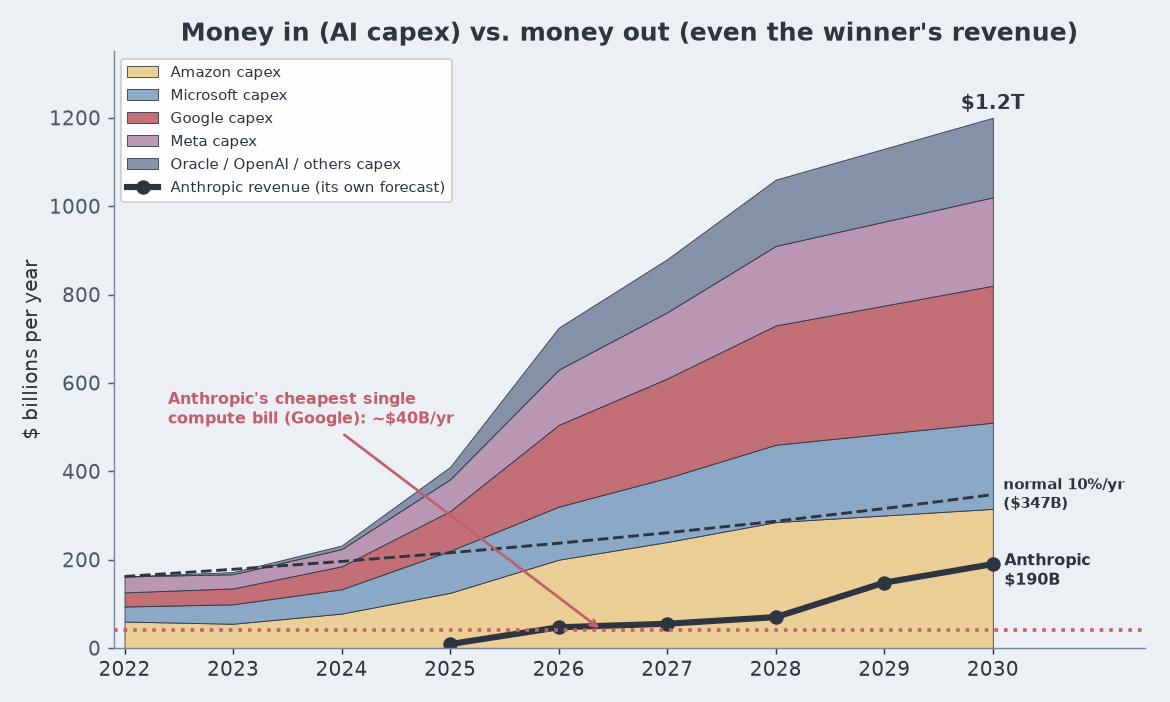

Money in (AI capex) versus money out (the winner's revenue, and the bill it cannot cover).

The five biggest spenders go from about $162 billion in 2022 to a planned $1.2 trillion a year by 2030; Goldman puts the four hyperscalers alone at $5.3 trillion cumulative for 2025 to 2030. Ordinary companies grow investment about 10% a year, which would land 2030 near $347 billion, not $1.2 trillion. The heavy line along the bottom is Anthropic's own revenue forecast, and the dotted line beneath it is roughly $40 billion, its single cheapest yearly compute bill: even the enterprise winner's whole income, and the one deal it most needs to cover, are slivers against a single year of capex. (Per-company splits are approximate; the totals, the Goldman figure, and Anthropic's forecast are the firm numbers.)

That heavy line is the one to watch, because Anthropic is not a laggard. It is the company winning the part of the market that actually pays: about 40% of enterprise LLM spend by the end of 2025 (Menlo Ventures), up from 12% in 2023 and ahead of OpenAI, used by roughly a third of businesses (Ramp), and holding a majority of the enterprise coding market. It grew revenue roughly tenfold a year, and its own best case still tops out near $148 billion in 2029, less than one seventh of that year's capex, and it is one company against the entire buildout. There is a harder ceiling underneath even that: Anthropic sells to enterprises, and there is a finite number of enterprises. It already has a third of them. You cannot grow tenfold a year for long against a market you are busy saturating, and when that growth bends, the capex line does not. The money going in keeps compounding after the money coming out has run out of new customers to find.

Put that dotted line in subscribers and it turns physical. Anthropic has committed more than $300 billion to compute: over $100 billion to spend on AWS, around $200 billion to Google and Broadcom, another $30 billion on Azure, against 2025 revenue of about $9 billion. Take just the Google slice, roughly $40 billion a year and its single cheapest commitment. Matched at OpenAI's $20 consumer seat, that one bill needs 167 million subscribers, more than three times every AI subscriber on Earth today. Matched at $200 a month, the Claude Max developer price, it needs 16.7 million developers, about 80% of the roughly 20 million professional developers on Earth, each paying Anthropic alone. And that is revenue matched one-to-one against one of three deals, with nothing left for the other $260 billion in commitments, for payroll, or for training the next model. Neither number exists, and the winner cannot price its way out: raise the seat and the base shrinks, cut it and the hole widens. That is what the dotted line meant.

And there is one more thing about the money going in: increasingly, it is not equity, it is debt collateralized by the money coming out. Oracle signed a $300 billion, five-year commitment to supply OpenAI with compute, financed with tens of billions in fresh debt a year, for a customer that loses money and can pay only as long as it keeps raising capital. Oracle's own annual filing now says the quiet part: "Our business is, and may continue to be, exposed to risks of customer non-payment and non-performance." Its stock fell more than 40% in a month, and in March 2026 the flagship Stargate campus in Abilene quietly scrapped its planned expansion after the financing talks collapsed. When the money in is borrowed against the money out, the gap in that chart stops being an investor's problem and starts being a creditor's.

And Oracle is not the outlier; it is the pattern. The big hyperscalers issued $121 billion of bonds in 2025, against a 2020 to 2024 average of $28 billion a year, Meta's $30 billion October sale the largest corporate bond of the year, and BofA expects $175 billion more in 2026, on top of tens of billions raised off balance sheet through private-credit vehicles. Worse, a growing share of the demand that justifies the borrowing is circular. Nvidia commits up to $100 billion to OpenAI; OpenAI commits $300 billion to Oracle; Oracle spends it on Nvidia chips: the cash leaves Nvidia's balance sheet as an investment and comes back as revenue. SoftBank sold its entire Nvidia stake to fund its $40 billion OpenAI commitment, selling the shovel-maker to finance the digger. And the loop is already creaking: Nvidia's OpenAI investment reportedly stalled in February 2026. When the buildout's biggest customer is financed by the buildout's biggest supplier, the demand signal the whole bet is priced on is partly its own money, going around in a circle.

The bull has one real answer to this, and it is not consumer subscriptions. It is that the value shows up as enterprise productivity, not $20 seats. Hold that thought. We will come back to it, because it is the hinge the whole bet swings on.

Run the numbers

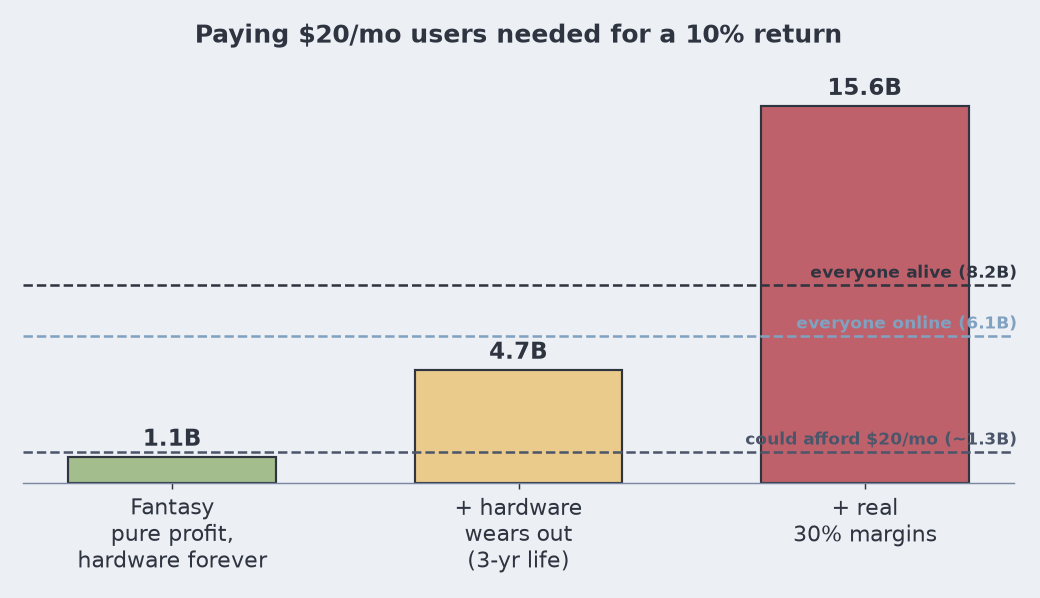

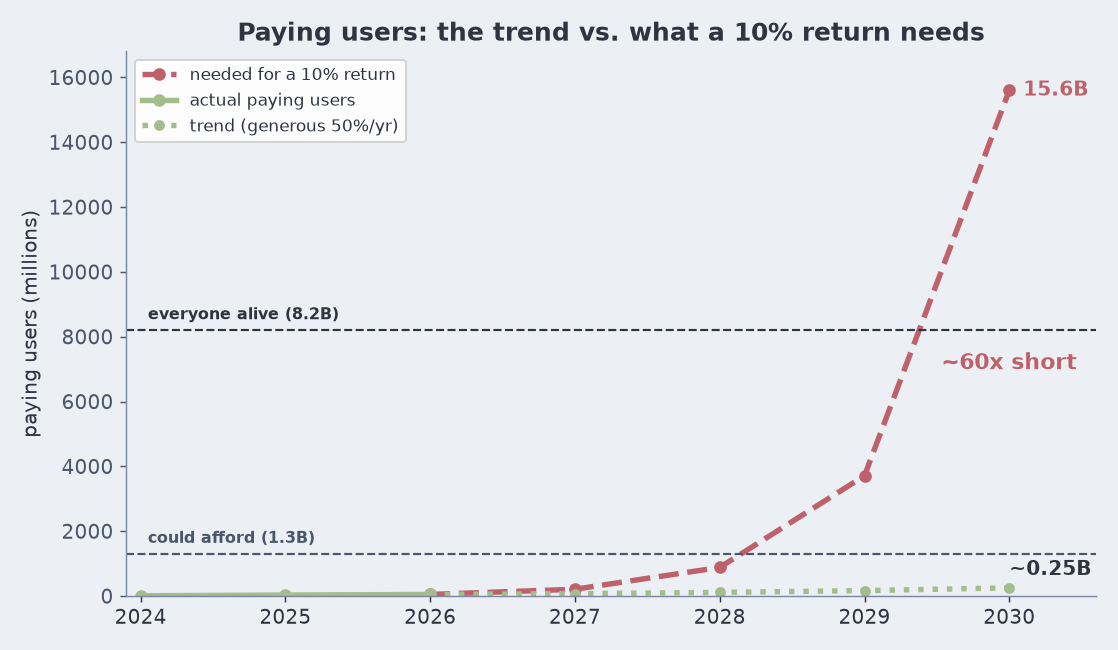

The funnel tells you who pays. The harder question is what it would take for them to pay it back. The arithmetic is simple: the number of $20-a-month users you need is the capital times your target return, divided by the annual profit per user. Give the bull everything. Treat the whole $2.59 trillion as a one-time investment, not an annual spend. Treat the full $240 a year per user as pure profit, no cost to serve.

Even in that fantasy, to earn a plain stock-market return of 10% you need 1.08 billion paying users: the entire current userbase, every one of them converted, at zero cost. That is not the ceiling of the estimate. That is the floor, the most generous case that can be constructed.

Now add one fact you cannot argue with. The GPUs depreciate to nothing in about three years, so you keep re-buying the $2.59 trillion. This is not an accounting opinion, the market is already marking it: GPU rental rates have fallen 50 to 70%, and billions in loans are collateralized by exactly those melting chips. Hold the target at that same 10% and the number jumps to about 4.7 billion payers, more than three-quarters of everyone online, still at pure profit.

Now add real margins. Every query burns compute and power, so call it a healthy 30%. At that point every target needs more paying customers than there are human beings. A plain 10% return wants about 15.6 billion users, 1.9 times everyone alive and more than 300 times the number who pay today.

And there is a harder ceiling than headcount: money. Only about 1.3 billion people could plausibly afford a $20-a-month discretionary subscription at all, roughly the 16% of the world that lives on $20 a day or more. For scale, the two largest consumer subscriptions on Earth, Netflix and Spotify, have only ever reached about 325 and 293 million paid. So the fantasy bar already needs nearly everyone who could pay, and the realistic bars need several times more paying customers than could ever exist.

Paying users needed for a 10% return, one dose of reality at a time, against the ceilings of who could ever pay.

And that 30% margin is generous, because it assumes the labs make money serving users at all. At the company level they do not. OpenAI posted about a 33% gross margin in 2025 and, on its own projections, burns roughly $25 billion in 2026 and does not expect positive cash flow until 2030, some $665 billion of cumulative burn along the way. Anthropic, the nearest thing to a counter-example, still spends far more than it earns once its compute commitments are counted. Both price access below blended cost on purpose, to buy market share. A single token may be sold at a profit; the business around it is not. Put a negative margin into the arithmetic and the red bar has no top at all: no number of $20 subscribers repays a company that loses money before scale even enters the question.

And the trajectory makes it concrete. Paying users have grown fast but from a small base, and already decelerating: roughly 10 million in 2024, 30 million in 2025, and about 50 million in 2026 (rough all-vendor estimates). Extend that at a generous 50% a year and you reach about a quarter of a billion by 2030. To earn a 10% return on the same clock you would instead need to grow paying users about 4.2x every year, 320% a year, for four years running to reach 15.6 billion. The two lines do not converge, they diverge: on trend you land roughly 60 times short, and you cross the ceiling of people who could even afford it long before that.

Paying users on trend, versus what a 10% return demands. There is no growth rate that closes it.

Which leaves exactly the exit the bull already reached for: enterprise seats at many times $20, not consumer subs. So the whole bet lands back on enterprise productivity being real, which is the one thing the measurements keep failing to find (next section). The two exits are the same door, and it is shut. One honest caveat: this treats $2.59 trillion as a one-time capital base; if it is genuinely annual recurring spend, the picture is worse, not better.

Why we are spending it

The spend is not madness. It is the second half of a fifty-year deal finally coming due.

For half a century the arrangement was: general hardware, specific software. One kind of chip, the general-purpose CPU, ran whatever you wrote on top of it. Software "ate the world" precisely because the hardware was general. You never had to build a new chip for a new app. And you would have been a fool to try, because Moore's Law and Dennard scaling made general chips faster every year for free. By the time you taped out custom silicon, next year's CPU had caught up. The software/hardware split was never a law of nature. It was an economic artifact of free hardware gains.

That subsidy expired. Dennard scaling ended around 2006, Moore's Law is crawling, clock speeds plateaued. Sutter called it in 2005: the free lunch is over. And once the general substrate stops getting faster for free, the only remaining way to buy performance is to specialize, to push the workload down toward the metal and etch it in. Hennessy and Patterson named the era in their 2018 Turing lecture, "A New Golden Age for Computer Architecture," and the thesis was blunt: domain-specific architectures are the future because general-purpose scaling is dead.

Software and hardware were only ever the same thing seen at two zoom levels, and where you draw the line between them is a choice, not a fact:

| Where the work lives | Flexibility | Speed and efficiency |

|---|---|---|

| Interpreted (Python) | highest | lowest |

| Compiled (C, Rust) | high | higher |

| Microcode | low | high |

| FPGA | very low | very high |

| ASIC (TPU, tensor core) | none, it is fixed | highest |

An FPGA is the proof: you "write software" (HDL) that becomes the circuit. An ASIC is that made permanent. The same function slides all the way down, trading flexibility for speed, and nowhere on the slope is there a natural seam where software stops and hardware starts. The AI buildout is the whole industry sliding down that table at once, betting that dense matrix math is the new universal primitive, worth freezing into silicon the way we once froze floating point.

That is the bet. Specific hardware for specific software, at planetary scale. And it is a leveraged bet, because it only pays if the workload it is carved for stays the workload.

Why it might not pay

Two cracks. Neither requires anyone to hate AI.

The productivity is measured with a broken ruler. The enterprise case, the hinge from earlier, rests on AI making people dramatically more productive. But we measure that with the metrics AI inflates for free: lines of code, pull requests, features shipped, velocity. Those were always bad proxies; they worked only because a human wrote each line, so "produced" quietly implied "understood." AI severs that link. Measure the thing that actually matters, correct and maintainable output, and the gain thins out or inverts. METR found that developers felt about 20% faster with AI and were measurably slower, because the time saved typing was lost auditing plausible, confident, wrong output. A 2026 NBER survey of nearly 6,000 firms found more than 80% reporting no impact on productivity or employment over the past three years. This is Goodhart's Law at civilization scale: we are pricing trillions in silicon on a number the tool can game.

AI breaks the economics of software. The reason software prints money is zero marginal cost: build it once, serve the next million users for nothing, keep 80% margins. AI does not work like that. Every query burns real compute and power, so cost-to-serve does not vanish with scale, it grows with it. Priced like software, it costs like a smelter. That is why the sector loses money at a billion users, with inference sold below cost and token prices falling. The $20 is a sticker price, not a profit.

And you cannot grow your way out of it. Software's escape hatch was always scale: the second million users cost almost nothing to serve, so growth diluted the fixed cost and margins widened as you got bigger. AI runs the tape backwards. Serving 100 times the users takes on the order of 100 times the GPUs and the megawatts, so growth multiplies the variable cost instead of diluting it. The treadmill speeds up as you run. There is no size at which the economics quietly turn, which is exactly why the buildout keeps needing more capital, not less, the more people use it.

There is a tempting third crack, that the models don't "really think," and it is the weakest one, so I will keep it to a sentence. The honest, sourced version is narrower and sharper: their reasoning is brittle pattern-matching that collapses off the training distribution, and the internal structure that looks like a world model is, on inspection, a bag of heuristics, used but not understood. Which matters here only because it is why the output has to be audited by a human every time, since you cannot reliably have AI check AI, which is why the productivity gain keeps not showing up in the measurements. The cracks are the same crack.

The part that should worry you

Whichever way the bet breaks, the consumer already lost the first round.

For forty years the consumer was the protagonist. The industry optimized for you, because you were the biggest market, and that pull dragged prices down every year. That era is over, not because computers got worse, but because you stopped being who they are built for. The frontier, the best fab nodes, the capex, the talent, the memory supply, has been redirected to AI. And the supply chain now bids against you: memory reallocated to datacenters is why consumer RAM prices are climbing right now. Your workload, browsing and email and a spreadsheet, got good enough on a six-year-old laptop and stopped asking for more. AI's workload is bottomless. R&D follows the bottomless one.

And this warning no longer comes from skeptics on the sidelines. The Bank for International Settlements, the central bank of central banks, used its June 2026 annual report to list an AI bust among the top threats to global prosperity, and its reasoning is precisely the structure above: capex outrunning earnings and free cash flow, every firm making the same bet at once ("firms over-committing resources to investment projects with still uncertain returns, leaving all firms vulnerable to disappointments in AI payoffs"), direct-lending funds that have quadrupled their AI exposure in five years, and circular deals that risk "the same asset being pledged multiple times." Its historical file for this shape: the canal mania of the 1830s, the railway mania of the 1840s, the electrification exuberance of the roaring twenties, the dot-com boom, each "a genuine technological breakthrough that attracted capital in excess of what commercial returns could ultimately justify," and each ending, in the BIS's own words, in an economy-wide recession. The first round cost you cheap hardware. The second is wired into the credit system.

Here is the twist, and it is the reason the bet is worth watching rather than fearing. No software paradigm has ever been the forever thing. The internet's plumbing, TCP/IP, survived, but everything built on top of it churned continuously; the applications were rewritten every few years while the substrate held. That is the argument against freezing today's paradigm into silicon. If transformers get dethroned, or the economics simply never close, the specialized hardware strands, exactly the way Lisp machines did in the 1980s when general-purpose workstations ate them. And when specialized silicon strands, the flexible, general substrate reasserts, because it can do everything cheaply. The fire-sale GPUs and the memory glut that follow a bust would hand cheap, powerful hardware back to the consumer who just got dethroned. The bust is the consumer's revenge.

What to actually watch

I am not calling the top. Betting the fab on matmul might be right; dense linear algebra is a far broader primitive than Lisp ever was, and it underlies graphics and simulation and every flavor of machine learning, not one paradigm. The honest position is two-sided, and the tells are numeric, not vibes:

- Token prices and inference-versus-training economics. Falling prices with no revenue growth is the overbuild signature.

- Datacenter utilization, cancellations, and delays. Stranded capacity shows up here first, and this tell has already fired once: the Abilene expansion was cancelled in March 2026.

- Hyperscaler debt issuance and the spreads on it. The buildout has shifted from cash to borrowed money, and credit spreads are where doubt prices in first. Per the BIS, the spreads of some AI firms have already begun to widen while equities still price the upside.

- The circular deals. Vendor-financing loops book demand that evaporates when they unwind, and Nvidia's $100 billion OpenAI investment reportedly stalled in February 2026.

- Enterprise productivity measured, not surveyed. If the real gains never arrive, the revenue that justifies the compute never arrives.

- The memory cycle. Structural demand shift, or an ordinary spike that fabs resolve.

The reason to keep the boring funnel in view is that it frames all of it. We are spending $2.59 trillion a year, more and more of it borrowed, to serve, at the paying end, about 50 million people, on the theory that a productivity miracle nobody can yet measure will show up to close the gap, for a software paradigm that history says will not be the last one. Maybe it does. But that is the bet, stated plainly, and it is a much bigger one than "AI is useful."

Read next